Podcast: Play in new window | Download

Subscribe: Apple Podcasts | RSS

In this episode, we ask:

- What is the history of Bank on Yourself®?

- What did Nelson Nash find with the Infinite Banking Concept?

- How was Nelson an evangelist?

- What’s the issue with the IBC meaning?

- What standards are in place around the Infinite Banking Concept?

- What did Pamela Yellen learn?

- What does Pamela write on page 247 of the Bank of Yourself® Revolution?

- What is a modified endowment contract (or MEC)?

- How did Pamela Yellen develop the Bank on Yourself® Professionals program?

- How is the Bank on Yourself® language protected?

- What is Bank on Yourself®?

- How does this make a significant difference?

- How might you know if an agent is capable and properly trained in designing a Bank on Yourself® type policy?

- What about investment advisors?

- What about designing riders properly?

- How are these policies different from traditional whole life policies?

- What is the only kind of insurance recommended for the Bank on Yourself® strategy?

- What about captive agents?

- What sort of products are captive agents writing?

- Does it sound too good to be true?

- What is Bank on Yourself® based upon?

- Who owns Bank on Yourself® type life insurance policies?

- Who do you know who is a Bank on Yourself® policy owner?

- Can that advisor truly help you?

- Why didn’t that advisor already tell you about Bank on Yourself®?

- What is Bank on Yourself® NOT?

- What about the knock-off advisors?

- What about advisors who lost their licenses?

- What is happening in the marketplace landscape?

- What about the Infinite Banking Concept?

- What about Private Banking Systems, Family Banking, Circle of Wealth, What Would the Rockefellars Do? and Perpetual Wealth Strategy?

- Have you heard episode 95 and 96?

- When was Nelson Nash’s Becoming Your Own Banker written?

- What’s wrong with outdated numbers?

- Is it about rate of return?

- Is it legal to call an insurance policy a “bank”?

- What about the laws and regulations?

- Did Nelson Nash defend his trademarks?

- How much do we treasure Nelson’s legacy?

- What is a 770 Account?

- What about the other names for a 770, including a President’s Secret Account, a 501(k) Plan, an Invisible Account and Income for Life?

- What about a 702(j) Retirement Plan, attributed to President Ronald Reagan?

- How are the Bank on Yourself® Professionals different?

- What about Wealth Beyond Wall Street?

- What is the promise?

- What are some other names?

- What is a Safe Money Millionaire or a 101 plan?

- What is Indexed Universal Life?

- What is in the fine print?

- What about the warnings and disclaimers?

- Why does the cash value on these go to ZERO?

- What about the watchdog investigation?

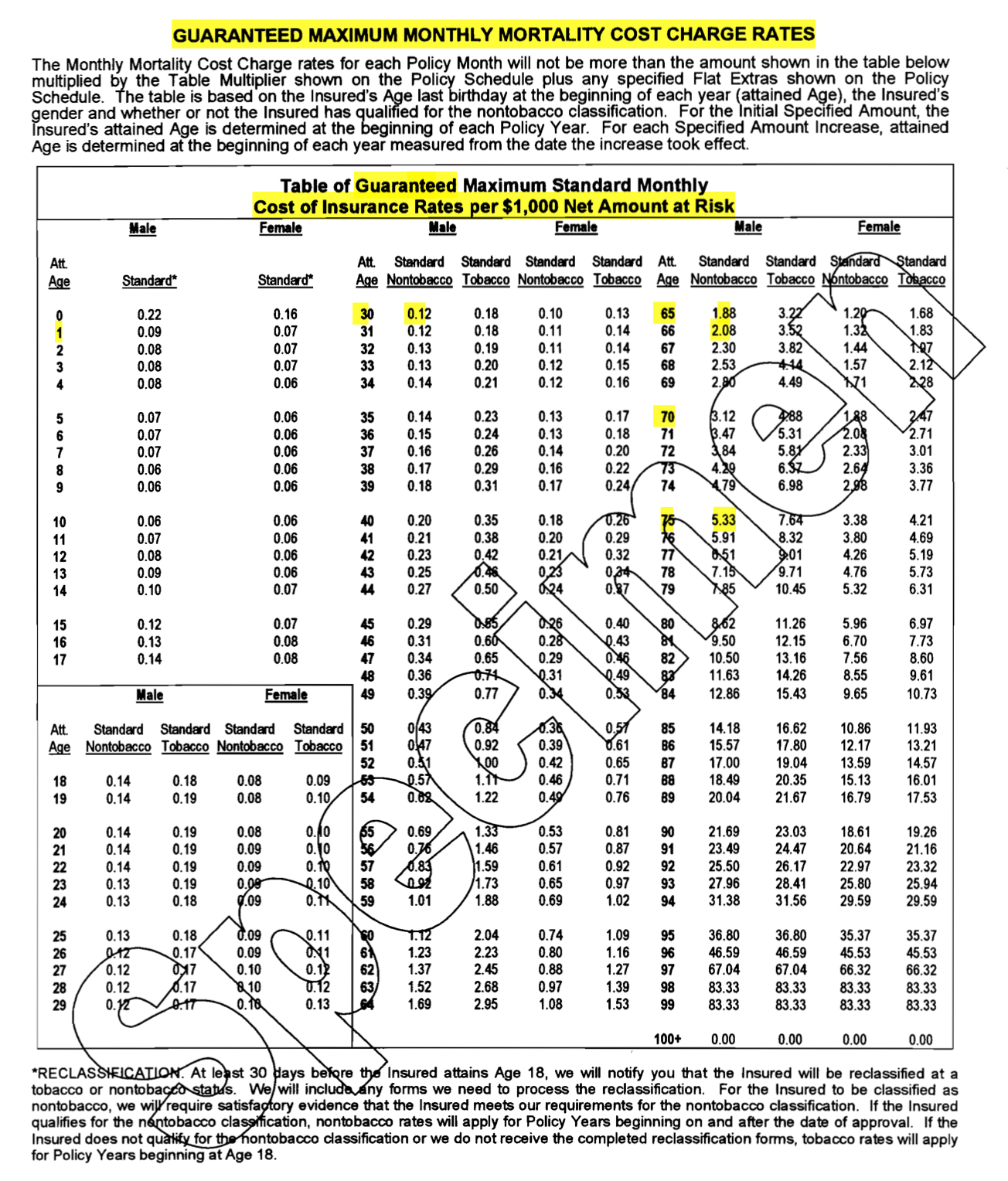

- Why are the illustrations on IUL and UL products wildly inaccurate?

- What are IUL problems?

- What about the IUL increasing costs?

- Why is this devastating?

- Why do these policies fall apart?

- Would you like to hear Episode 59?

- Would you like to hear Episode 60?

- Would you like to hear Episode 61?

- How are Bank on Yourself® Professionals different?

- What is Maximum Premium Indexing and why is it so hot right now?

- Why are they recommending buying an IUL and a whole life policy?

- What is this mysterious strategy?

- What is the advantage? What is the downside?

- What is piggy backing?

- Who does this benefit?

- What are the red flags?

- Why is this an ethical crisis?

- Why is borrowing from one policy to buy a new one a bad idea?

- What can you do if you’ve already purchased an inefficient or troubling policy?

- Have you heard of the 1031 exchange in real estate?

- Is there a like kind exchange in insurance?

- What is the 1035 exchange?

- Do you have an in-force illustration?

- Would you like to call your insurer to get an in-force illustration?

- Would you like us to review your in-force illustration for FREE?

- Email us your PDF at hello@nyafinancialpodcast.com

- or hop on Mark’s calendar.

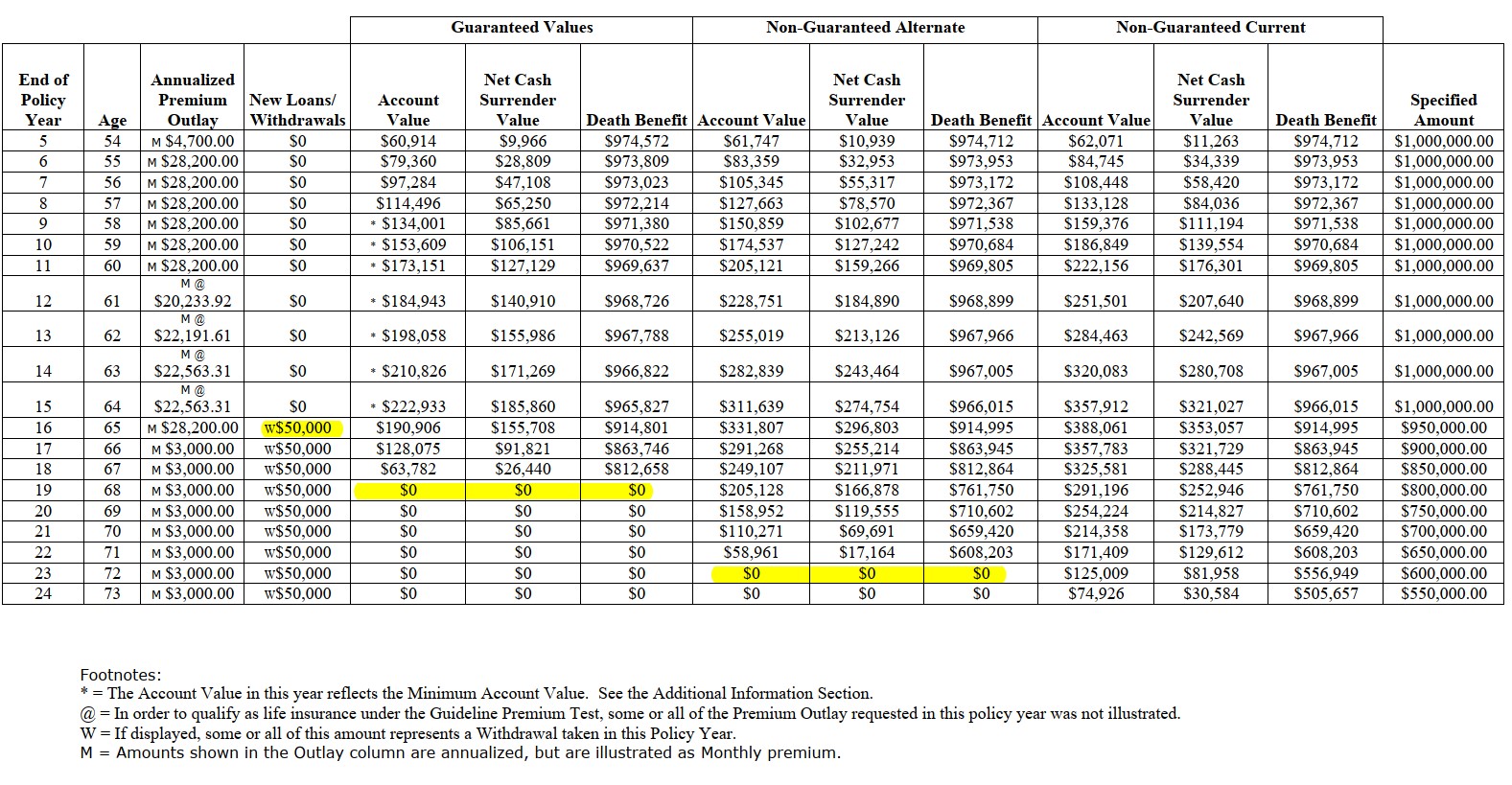

The Problem with Costs Going Crazy in Indexed Universal Life (IUL)

Example of What Might Happen with Retirement Income Using Indexed Universal Life (IUL)

As Chief Distribution Officer of Foresters Financial, Matt Berman is responsible for life insurance and annuity product development, pricing and sales across the United States and Canada.

As Chief Distribution Officer of Foresters Financial, Matt Berman is responsible for life insurance and annuity product development, pricing and sales across the United States and Canada. Matthew Shanlian received his bachelor’s degree in finance from Liberty University before working full time in the mortgage industry starting in 2007. Matt began as a Loan officer assistant and has worked his way up to Division President with Primary Residential Mortgage, INC. Matthew is a nationally recognized speaker, frequent podcast guest, and also serves on the board of directors for NIME, a non-profit , financial services education organization. These activities have helped him earn the achievement of being ranked by Mortgage Executive Magazine as a Top 1% Mortgage Originator in America. In his time away from the office, Matthew loves serving in his local church’s children’s ministry with his wife, Maria. Together they have 3 children, Miles, Millie, and Maverick.

Matthew Shanlian received his bachelor’s degree in finance from Liberty University before working full time in the mortgage industry starting in 2007. Matt began as a Loan officer assistant and has worked his way up to Division President with Primary Residential Mortgage, INC. Matthew is a nationally recognized speaker, frequent podcast guest, and also serves on the board of directors for NIME, a non-profit , financial services education organization. These activities have helped him earn the achievement of being ranked by Mortgage Executive Magazine as a Top 1% Mortgage Originator in America. In his time away from the office, Matthew loves serving in his local church’s children’s ministry with his wife, Maria. Together they have 3 children, Miles, Millie, and Maverick.

Gene Guarino is the founder of the

Gene Guarino is the founder of the  Jim Cockrum & his team have been on a mission, since the 90s, to help entrepreneurs THRIVE by combining classic business truths with cutting edge creative online strategies. They now boast over 1,000 documented success stories from entrepreneurs and businesses around the world, but they are just getting started!

Jim Cockrum & his team have been on a mission, since the 90s, to help entrepreneurs THRIVE by combining classic business truths with cutting edge creative online strategies. They now boast over 1,000 documented success stories from entrepreneurs and businesses around the world, but they are just getting started!