Podcast: Play in new window | Download

Subscribe: Apple Podcasts | RSS

In this episode, we ask:

- When I say the word rider, what comes to your mind?

- What about riders on legal documents?

- What is the legal definition?

- How does life insurance deal in the world of contracts?

- What are augmented, modified whole life insurance contracts?

- Have you heard Episode 6?

- How do certain riders maximize growth?

- What is the storehouse?

- What is the new way of thinking about life insurance?

- What is the old way of thinking about life insurance?

- What is the question?

- What one rider is so unique and powerful?

- What’s a paid-up additions (PUA) rider?

- How is the PUA rider so powerful?

- How is a PUA rider like making an addition onto a house?

- How do PUAs add value to the contract?

- Who understands PUAs?

- How are PUAs tiny but mighty?

- What do insurance agents learn during training?

- What do most insurance agents overlook?

- How do PUAs engage compound growth?

- What about flexibility?

- What about skipping a year?

- What about increasing when ready?

- What sort of possibilities do PUAs offer?

- How do PUAs interact with the base premium?

- How do PUAs work in a Bank on Yourself type whole life insurance policy?

- What about dividends?

- What about compounding?

- What’s an age-specific example?

- What about market risk?

- What about Dave Ramsey’s and Suze Orman’s concerns?

- How is this different from what they’re talking about?

- Why is it a bad idea to conceptually lump all life insurance together?

- How is a PUA like a deposit?

- How much cash value is immediately available?

- Why not put all of the premium into a PUA rider?

- Why can’t PUAs exist on their own?

- How is this like a sailboat?

- What would it be like to have only a sail?

- What gives a sailboat power?

- Where do the biggest dividends come from later in life?

- How does the blend work?

- Where is the balance?

- How is it like a seesaw on the playground?

- How is a policy structured properly?

- What is the best design?

- How is a policy like a hamburger?

- Is there a one-size-fits-all recipe?

- How are the ratios considered?

- How does age affect design?

- How does time affect design?

- Do you have someone to design something with your specific concerns in mind?

- Are there more riders?

- What are the PUA riders?

- How might you add PUAs?

- What benefits do PUAs provide?

- How do PUAs grow?

- What about interest?

- What about dividends?

- What is the key?

- Do you have this rider on your policy?

- Do you wonder if you have PUAs?

- Would you like a review of an existing policy? Reach out for a 15 minute phone call

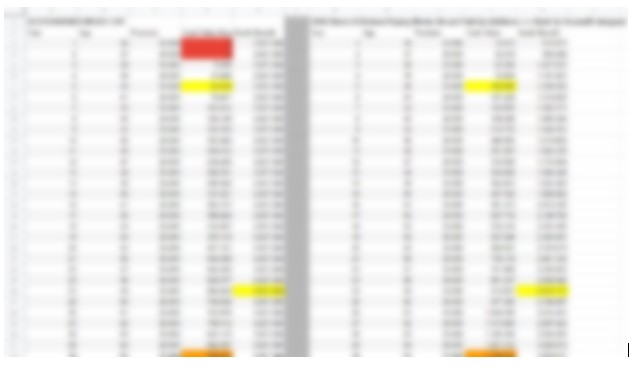

In this episode, we mentioned a visual spreadsheet on the difference between Old-Fashioned Whole Life, and Bank On Yourself ® type Whole Life, designed for maximum cash value. Want to see the numbers in action? Sign up here to get them!

Old Fashioned Whole Life vs. Bank On Yourself Designed Whole Life 40/60