Podcast: Play in new window | Download

Subscribe: Apple Podcasts | RSS

In this episode, we ask:

- Who is Frank Herbik?

- How did Marvin Bulas get started with Tim Austin?

- What does the concept of Bank on Yourself® focus upon?

- Do you rely on other outside financial sources?

- What requires self-discipline?

- How can you achieve your financial milestones without taking unnecessary risks?

- What about discipline and freedom?

- Have you read Extreme Ownership by Jocko Willink?

- How about a lifetime of tax-advantaged income?

- What is hard?

- How does the Bank on Yourself® strategy differ from a typical market-driven approach like a mutual fund, an ETF, an IRA, etc.?

- How about some examples?

- Are we completely against the market?

- What is the barbell strategy?

- What about a better “desk drawer”?

- How can you harness compound growth?

- What about cash, that’s available to you, whenever you need it?

- Could everyone benefit from this?

- How does the insurance carrier manage and carry the risk?

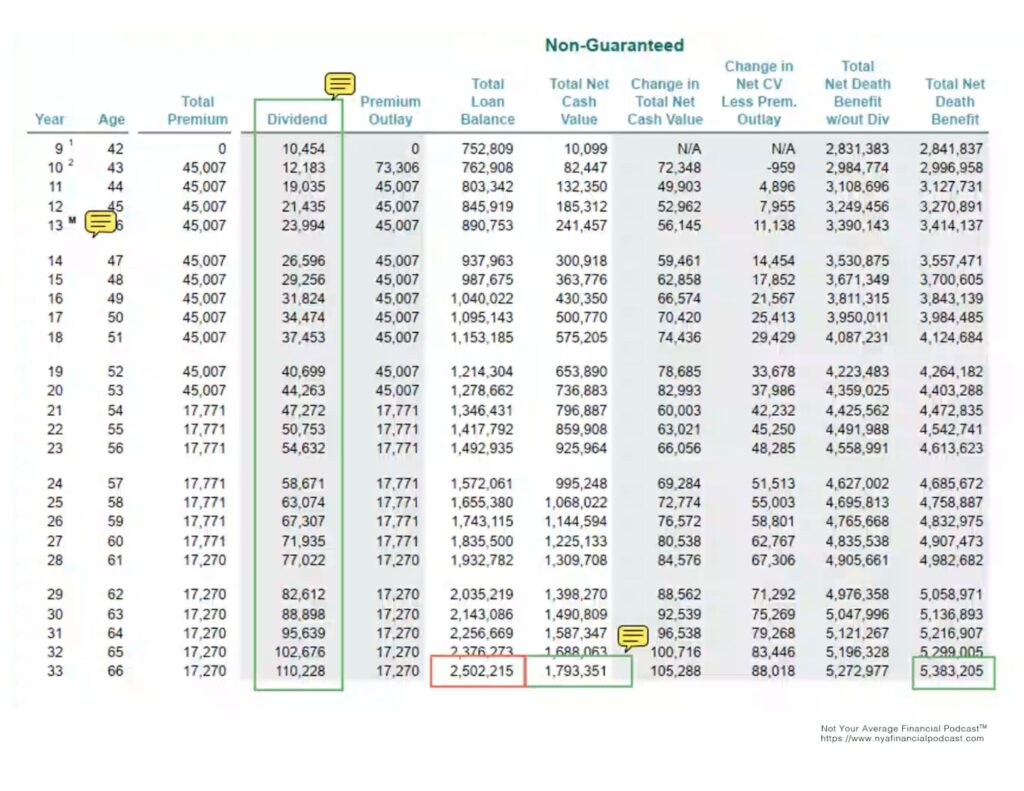

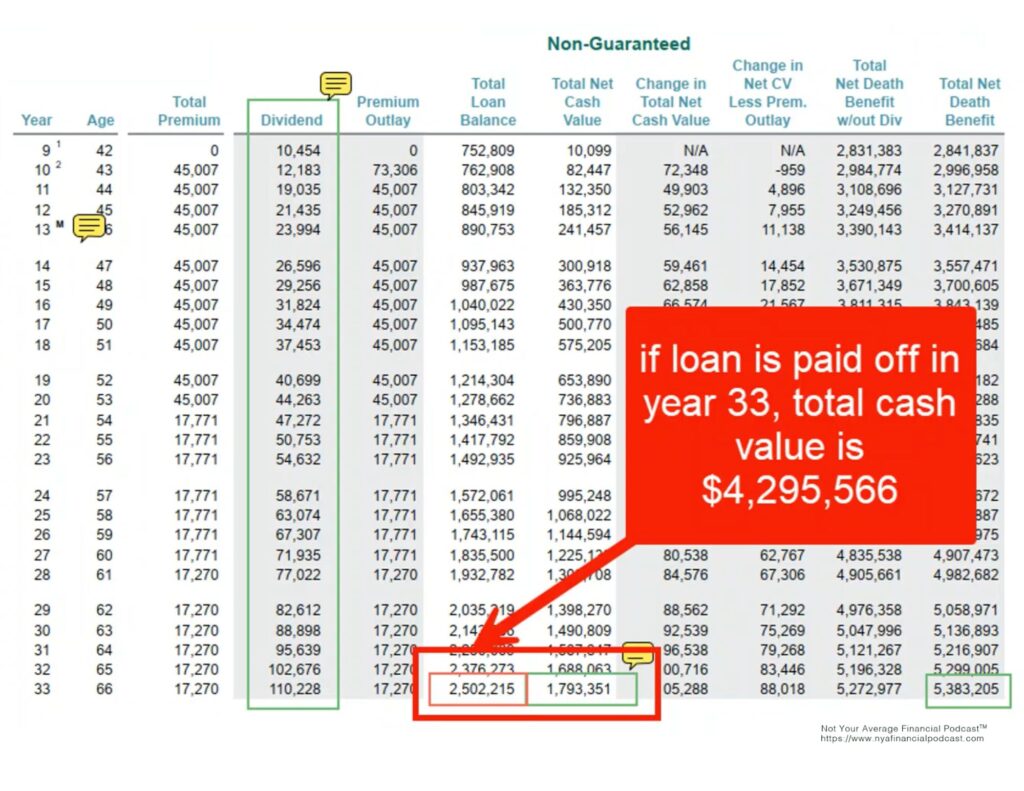

- What is the non-guaranteed component?

- Are the companies in the insurance industry well regulated?

- What are the living benefits?

- What’s the difference between a typical life insurance agent and an active Bank on Yourself® Professional?

- What’s the CFP® designation?

- Does a typical CFP® (or CLU®) understand how to correctly structure and design a Bank on Yourself® type whole-life insurance policy?

- What does Marvin enjoy?

- What can smooth out a lot of things?

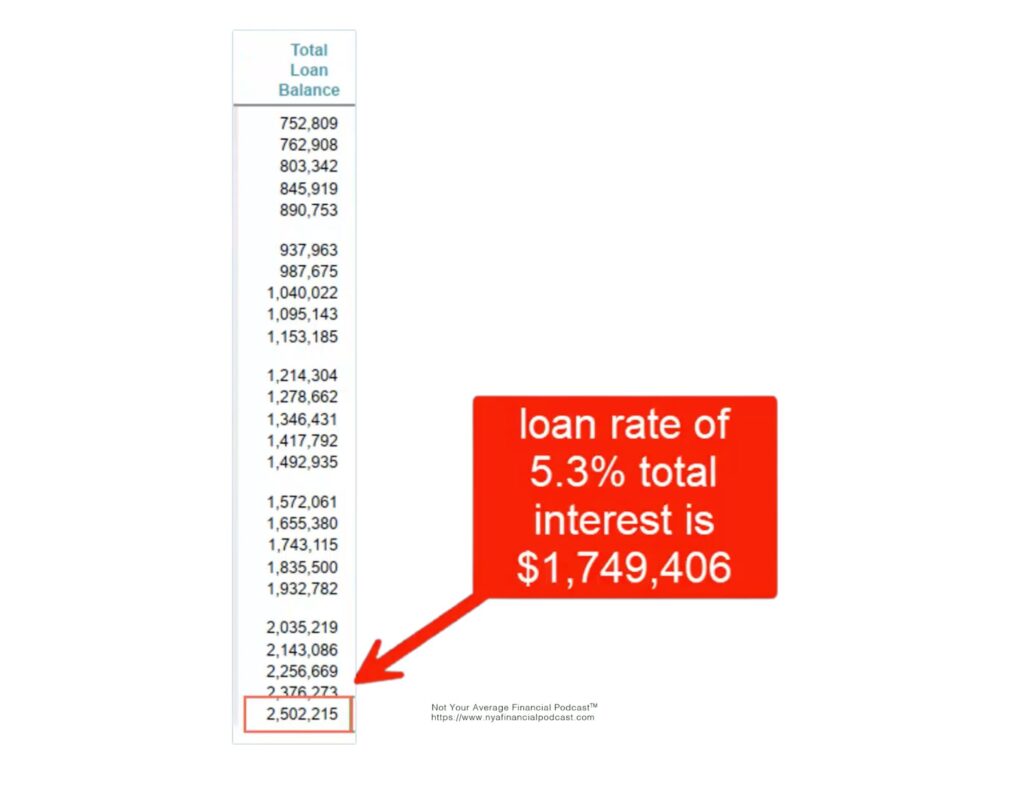

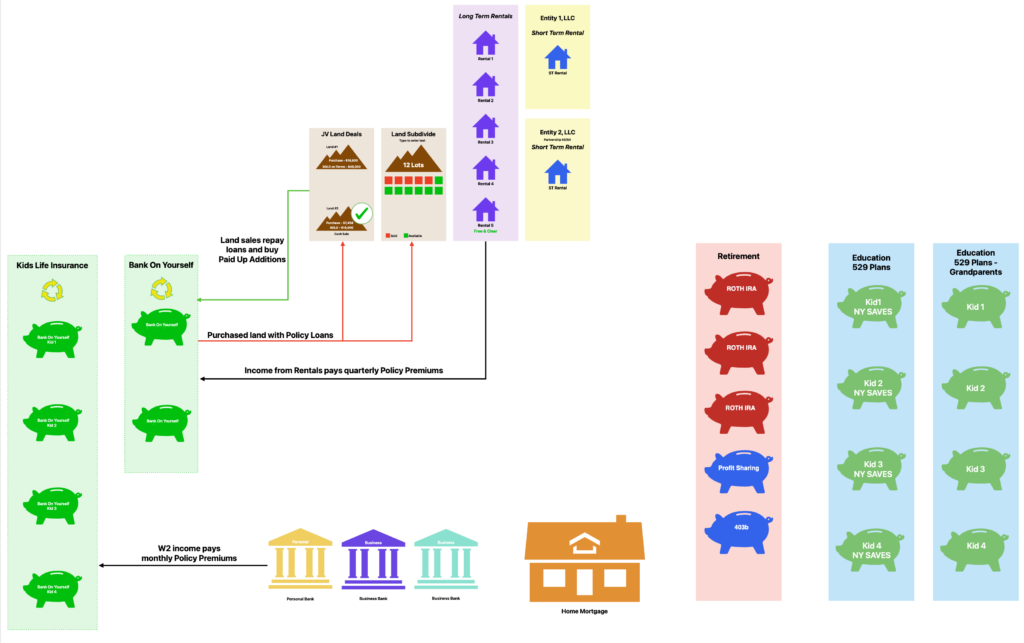

- How about a case study?

- What is the approval process to get a loan from an insurance carrier?

- How much do you want, and when do you want it?

- Who sets the terms of the loan?

- What resonates with Frank?

- Do carriers have apps?

- Who would these concepts benefit?

- How does age affect the growth of a whole life insurance policy?

- What is a “sprinter” policy?

- What is a “marathon” policy?

- How many ways could an advisor design a policy?

- Would you like to search on bankonyourself.com?

- Would you like to talk with Frank at 630-330-1799 about your specific situation?

Matthew Shanlian is the Vice President of Lending for Crosscountry Mortgage, LLC. the Largest independent mortgage bank in the United States. For the past 15 years, he has focused on educating and supporting the financial services industry and their clients. Matthew travels the country to train financial professionals on Strategic Equity Planning for their clients. He believes that the having a plan for your home is paramount to a building wealth.

Matthew Shanlian is the Vice President of Lending for Crosscountry Mortgage, LLC. the Largest independent mortgage bank in the United States. For the past 15 years, he has focused on educating and supporting the financial services industry and their clients. Matthew travels the country to train financial professionals on Strategic Equity Planning for their clients. He believes that the having a plan for your home is paramount to a building wealth.

Max Brusky is an attorney specializing in civil litigation, particularly insurance defense, coverage, and subrogation. He is currently an “in-house” and Claims Director for a national trucking company. He is a happy husband to a happy (and brilliant, and understanding) wife, and the proud father of two, one in college, one almost in college. He currently lives in Chicago’s far west suburbs, but still considers himself a Wisconsin expatriate.

Max Brusky is an attorney specializing in civil litigation, particularly insurance defense, coverage, and subrogation. He is currently an “in-house” and Claims Director for a national trucking company. He is a happy husband to a happy (and brilliant, and understanding) wife, and the proud father of two, one in college, one almost in college. He currently lives in Chicago’s far west suburbs, but still considers himself a Wisconsin expatriate. Mike Michalowicz is an investor, active partner in multiple companies and a prolific author. His bestselling book, Profit First, has sold more than one million copies.

Mike Michalowicz is an investor, active partner in multiple companies and a prolific author. His bestselling book, Profit First, has sold more than one million copies.

Dave Bonnemort is a current client and active practitioner of the Becoming Your Own Banker concept, as well as a husband to an amazing wife and father to three incredible kids.

Dave Bonnemort is a current client and active practitioner of the Becoming Your Own Banker concept, as well as a husband to an amazing wife and father to three incredible kids.